This blog post is the second in a series on the retail energy market in DC. The first post covers retail energy market trends and analysis and can be found here. The third post in the series is forthcoming and will report the findings from a randomized controlled trial to test the effectiveness of behavioral interventions among consumers in the DC’s competitive energy market.

Retail energy competition has produced mixed results in the DC market. Liberalization policies opened electric and natural gas supply markets to competition during the mid-to-late 1990s, and this, in turn, led to deregulation. As a result, residential customers in DC may choose between the default utility supply service and competitive retail supply service. However, local utilities must still provide transmission and distribution services for all customers regardless of their suppliers. As we explain here, deregulation of energy supply markets appears to benefit commercial customers in DC, on average, but not residential customers. Many suppliers appear to engage in price discrimination in the residential market by exploiting information asymmetries and inattention, especially among lower-income residents.1

According to a Wall Street Journal analysis using Energy Information Administration (EIA) data from 2021, residential electricity consumers nationwide paid $19.2 billion more than they could have paid had they purchased electricity from the default utilities in their states. This is consistent with findings from DOEE’s recent analysis of 14 months (July 2023 – August 2024) of residential and commercial electricity market data for DC. We found that residential customers of retail suppliers paid $17.85 million more during the period than they would have on the default electricity supply service from Pepco. Retail customers paid, on average, 70% higher prices for electricity supply than customers of Pepco’s regulated Standard Offer Service (SOS). Low- to moderate-income (LMI) residential customers, who received utility assistance during the period, paid an even higher premium – an average of 80% more – for retail electricity compared to customers of Pepco.

Many states with competitive supply markets have observed similar trends of price discrimination and consumer losses2 and have addressed these dysfunctions by passing reforms to curtail predatory practices and artificially high prices. To better understand the types of market reforms in other states, we conducted semi-structured interviews with state officials from Connecticut, Massachusetts, New York, Pennsylvania, and the United Kingdom (UK). We have kept our sources anonymous here but these individuals have all been instrumental in designing their states’ retail market reform policies as regulators, attorneys, or energy market analysts.

What did we learn from interviews with state officials?

We asked each state’s official(s)3 a series of questions to learn more about each of the topics listed in Figure 1 below. We used NVivo software to qualitatively analyze transcripts of the discussions. Our goal with transcript analysis was simply to identify common themes, record the frequency with which these themes are mentioned, and review specific issues other states have addressed with reform. We then used these themes to frame reform options for DC’s market.

Penalties and enforcement

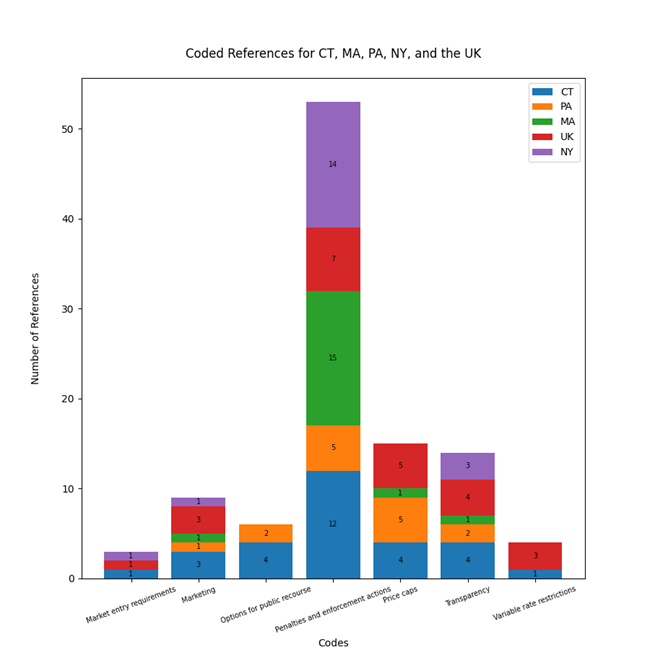

Perhaps unsurprisingly, the most frequent theme that was discussed among all state officials was the use of penalties and enforcement for suppliers that violate regulations. Officials from Massachusetts and New York mentioned penalties and enforcement most frequently. Specific penalties and enforcement actions discussed included regulators issuing warnings, levying fines, revoking operating licenses, and pursuing legal action. Ultimately, enforcing regulations and assessing penalties can create an administrative burden for regulators and lead to enforcement gaps, which means that relying solely on this policy lever is often insufficient and inefficient.

Market entry requirements

Strengthening market entry requirements for suppliers was also a major focus of conversations. Officials from New York, the UK, and Connecticut all touched on the importance of market entry requirements that may help deter bad actors prior to operation. For instance, to obtain an operating license, suppliers could be required to provide copies of all supply contracts to be shared publicly or with the regulator, provide detailed financial records to the regulator, share complaints or violations from other states in which the suppliers operate, and agree to regularly report operating data, including supply prices charged among customers. Connecticut requires a phone number and address for customer complaints and mandates that suppliers keep a record of complaints for a minimum of three years, available upon request. New York does not allow new supplier contracts unless they guarantee savings for the customer or the supply is generated from at least 30% renewable energy. Market entry requirements can help shape what types of services will be provided and guarantee some level of financial credibility of participating suppliers, but these requirements are unlikely to screen completely for bad actors and harmful practices.

Transparency

A desire for increased transparency between suppliers and customers was expressed often in the discussions. All states analyzed here have created electricity supply contract comparison websites, and some, including New York, also include natural gas suppliers’ contract options. Comparison sites advertise supply prices, contract types (e.g., fixed, variable, volumetric, non-volumetric), contract duration, and other contract details among different suppliers in a service area. New York’s Power to Choose website displays a consumer advisory alert when the page is first opened, warning users to exercise caution when comparing contracts and to compare contract price offers with the default supply price. DC Power Connect, which is hosted by DC’s Public Service Commission, serves a similar role but is completely voluntary for suppliers to advertise contracts. As a result, there are typically different contract options from only a fraction of the total number of operating suppliers in DC that advertise on the site, making it difficult to truly compare across all available options. Suppliers seem to rely more on telemarketing and door-to-door marketing for customer recruitment. If information asymmetries are one of the major drivers of inequities in competitive markets, transparency measures may help to narrow the information gap.

Marketing

Marketing practices have been a major focus of customer complaints and of market reform across states. From 2022 to 2025 in DC, OPC recorded 2,197 complaints of deceptive or abusive treatment by suppliers and their marketers. These complaints and others have led DC’s Office of Attorney General to issue a consumer alert to raise awareness about how to avoid scams and bad actors in the market.4 This phenomenon is not unique to DC, which has pushed some states to prioritize marketing reform measures. For instance, Massachusetts and Connecticut now require retail suppliers and their marketers to clearly explain all price and contract details, including comparisons to default prices, before customers can be enrolled.5 Marketing reforms may be necessary to protect consumers at the primary point of contact between customers and suppliers, but these regulations may not be sufficient in anticipating all ways in which customers could be deceived.

Variable-rate contract restrictions

Several states have decided to restrict or ban variable-rate contracts because these contracts allow suppliers to increase supply prices suddenly and sharply while trapping customers in contracts with prohibitively high termination fees. Connecticut banned variable-rate contracts in 2015, meaning suppliers are no longer allowed to change supply prices monthly. Maryland has also banned variable-rate contracts; additionally, Maryland requires suppliers to provide prior, written notice to customers when their contract renewal prices are set to increase. Automatic renewals of fixed contracts can allow suppliers to increase prices similarly to variable-rate contract structures, making it incumbent upon regulators to consider consumer protection in both instances.

Price caps

Enforcement of marketing practices can be costly in terms of time and resources. Understanding this challenge and the fact that many suppliers tend to offer very similar services, several states have implemented price caps that are tied to default supply pricing. Price caps often include some exceptions or special considerations for additional renewable energy or other novel or beneficial service offerings. For instance, in New York, a price cap mandates that no energy supplier charge more than the equivalent of the default utility’s charges on an annual basis, with the exception of green products that are certified by New York’s Public Service Commission. The UK has a more flexible price cap, which is adjusted by its regulator, Ofgem, as frequently as every three months to reflect different market input costs, including wholesale purchasing, network, operating, and industry debt costs.

In addition to states represented in our interviews, we also reviewed relevant reform measures proposed or passed in Maryland and Maine, including price caps. The Maryland State Legislature recently passed Senate Bill 1, which restricts suppliers from charging customers more than the average price of the local utility’s default price over the prior 12 months. Maryland does allow suppliers to charge more when meeting “green power” requirements.6 Maine does not currently cap prices, but its Office of the Public Advocate recommended capping prices at or below the default service price. In general, price caps may be one of the most effective policy levers to ensure consumer protection by limiting or eliminating price discrimination; however, price caps are also likely to limit innovation and service differentiation, which may need to be considered when allowing exceptions or relaxations of caps.

What should be done when competition leads to discrimination?

From a public policy perspective, there are several different prescriptive solutions, or combinations of solutions, that may address shortcomings of competitive retail markets, but these solutions can be categorized using one of two paradigms: “i-frame” or “s-frame” interventions. Coined by Chater and Loewenstein (2022), i-frame interventions rely on individuals to make responsible decisions following some form of educational or persuasive intervention (e.g., nudging individuals to enroll in retirement plans), whereas s-frame interventions are systemic in nature (e.g., federal law requires employers to automatically enroll employees in retirement plans). DOEE has carefully explored individual-level interventions to provide consumer protection information to customers directly. However, these interventions produced tepid and likely temporary results (See more from our randomized controlled trial in the forthcoming third post in this series). These findings underscore the urgency in pursuing systemic regulatory reform in DC’s retail energy market to lower cost burdens for customers.

Some states, such as Maryland, New York, and Massachusetts, have largely re-regulated residential supply markets, while other states, including the UK and Texas, have moved increasingly toward incentivizing competition with more or less guardrails built into the market. Some states have decided the best way to protect particularly vulnerable parts of the population is to exclude them from participating in retail choice. For example, Georgia, Florida, Nevada, Oregon, and Tennessee only allow retail choice in the commercial sector but not the residential sector. Connecticut, Maryland, New York, and Pennsylvania require low-income customers to remain on default supply services. New York only allows suppliers to recruit low-income customers if the suppliers can guarantee savings for customers. Clearly, there are consumer protection concerns7 when markets are less regulated, and the question is how best to protect consumers if states continue to allow competition.

DOEE’s recommended reforms for DC

Semi-structured interviews with state officials and background research on what other states have prioritized informed DOEE’s recommendations that we present in detail here and concisely below:

A price cap

- Retail suppliers may charge up to 10% above the prior 12-month average default supply price

- Exceptions to charge higher prices will be allowed for suppliers offering services determined to be in the public interest or additional renewable energy compared to what is required by DC’s RPS

More granular and regular data reporting from suppliers

Greater transparency requirements for suppliers, including publicly sharing all available contract options on the PSC’s electric supplier contract comparison website, DC Power Connect, and a corresponding natural gas website that is set to launch soon8

Elimination of early termination fees to allow residents to easily exit unwanted contracts

Thank you to Peter Damrosch and Andrew Held for their comments.

Footnotes

Some retail energy suppliers offer services that provide additional benefits that entice customers to pay a premium, such as additional renewable energy generation (for electricity) or bundled services. However, many retail supply contracts offer little additionality compared to default utility services. Furthermore – with regard to additional renewable energy as one of the clearer benefits of competition in retail electricity markets – the default electricity service provided by Pepco is required to become increasingly renewable in compliance with the renewable portfolio standard (RPS) in DC; currently, 59% of electricity sold in DC must come from both local solar generation (5% of the 59% total) and from other renewable energy generation or renewable energy credits (RECs). By 2032, 100% of electricity sold by all suppliers and Pepco will be derived from renewable sources, which suggests diminishing returns from competition if the main benefit is additional renewable energy consumption. We also note that, based on our analysis, additional costs associated with generating clean electricity do not explain most of the price premiums we observed.↩︎

Of course, it is also important to note that some customers choose to pay a premium for specific benefits, such as additional renewable energy generation in their electricity mix compared to the default mix or bundled services and perks, such as rewards programs or energy-efficient appliance discounts.↩︎

For some states, we spoke to multiple officials at once.↩︎

Specifically, complaints from residents have highlighted incidents of marketers posing as representatives of the local utility, pressuring residents to enroll, enticing residents with short-term “teaser rates” while hiding additional fees and high long-term rates, misrepresenting the type or amount of renewable energy offered, “slamming” (i.e. enrolling customers without consent or knowledge), and disregarding customers’ requests to end their contracts.↩︎

Maryland allows residents to join a “do no transfer list” that ensures customers stay with the default utility and are not contacted by marketers.↩︎

Green power suppliers are allowed to charge a higher supply price than the trailing 12-month average for the default utility service if they 1) provide renewable energy and/or RECs equivalent to at least 51% of what is required by Maryland’s RPS, and 2) Maryland’s PSC approves the prices offered by green power suppliers.↩︎

Notably, consumer protection tends to focus on the residential market, though small commercial customers have been shown to pay high price premiums in some markets as well. In New York, for example, small commercial customers are also protected under the price cap. Generally, larger commercial customers have fared relatively well in competitive markets. This may be due to various factors, including scale, greater market knowledge, etc.↩︎

The PSC is currently creating a contract comparison website for natural gas suppliers to post contract options.↩︎